Understanding the ABA Number is crucial for anyone who deals with bank transfers, direct deposits, or checks. This unique identifier ensures that your money reaches the right financial institution without any hassle. Let's explore what this number is, its purpose, and how it plays a significant role in the banking system.

Whether you're setting up a direct deposit for your salary or sending funds to another account, knowing your ABA Number can save you from potential errors. This article will provide you with a comprehensive understanding of ABA Numbers, including how they work and how to locate them on your checks.

As we delve deeper into the world of banking, it's essential to familiarize yourself with terms like ABA Number, which are fundamental components of the U.S. financial infrastructure. In this article, we will explore everything you need to know about ABA Numbers and why they are indispensable in today's digital banking landscape.

What is an ABA Number?

An ABA Number, also known as a routing transit number (RTN), is a unique nine-digit code assigned to financial institutions in the United States. It serves as an identifier for banks and credit unions, ensuring that funds are routed to the correct institution during transactions.

Why is the ABA Number Important?

The ABA Number is vital because it streamlines the process of transferring money. Whether you're wiring funds domestically or setting up automatic payments, this number ensures accuracy and efficiency in financial operations.

The History of ABA Numbers

The American Bankers Association (ABA) introduced the ABA Number system in 1910 to standardize the process of clearing checks. This innovation helped banks manage transactions more effectively, reducing errors and delays.

Evolution of the ABA Number System

Over the years, the ABA Number system has evolved to accommodate advancements in technology. From manual check processing to electronic transfers, the ABA Number remains a cornerstone of modern banking infrastructure.

ABA Number Format and Structure

An ABA Number consists of nine digits, each serving a specific purpose. The first four digits represent the Federal Reserve Routing Symbol, while the next four identify the bank or financial institution. The final digit acts as a checksum to validate the number's accuracy.

Breaking Down the ABA Number

- First Four Digits: Indicates the Federal Reserve Bank where the institution holds its account.

- Next Four Digits: Identifies the specific bank or credit union.

- Last Digit: Acts as a check digit to confirm the number's validity.

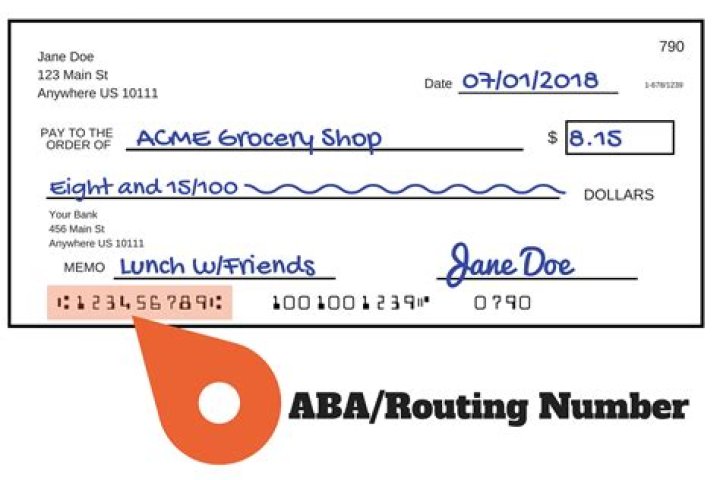

How to Find Your ABA Number

Locating your ABA Number is simple. It is typically found at the bottom of your checks, printed in magnetic ink for automated processing. Alternatively, you can find it on your bank's website or by contacting their customer service.

Where to Look for Your ABA Number

- On your personal checks

- Through online banking platforms

- By contacting your bank's customer support

Common Uses of ABA Numbers

ABA Numbers are used in various financial transactions, including:

- Direct deposits

- Wire transfers

- Bill payments

- Automated Clearing House (ACH) transactions

How ABA Numbers Facilitate Transactions

By providing a standardized method of identifying financial institutions, ABA Numbers ensure that funds are directed to the correct accounts, minimizing the risk of errors and delays.

Difference Between Routing and ABA Numbers

While the terms "routing number" and "ABA Number" are often used interchangeably, there is a subtle distinction. A routing number is a broader term that includes both ABA Numbers and ACH Numbers. ABA Numbers are specifically used for paper transactions, such as checks, while ACH Numbers are utilized for electronic transfers.

Key Differences

- ABA Numbers: Used for paper-based transactions

- ACH Numbers: Used for electronic transactions

ABA Number Security and Privacy

Protecting your ABA Number is essential to safeguard your financial information. Sharing this number with unauthorized parties can lead to fraudulent activities. Always verify the recipient's identity before disclosing your ABA Number.

Tips for Securing Your ABA Number

- Limit sharing to trusted entities

- Monitor your accounts for suspicious activity

- Shred documents containing your ABA Number

Common Mistakes to Avoid with ABA Numbers

Errors in entering or sharing ABA Numbers can result in failed transactions or misdirected funds. Some common mistakes include:

- Transposing digits

- Using outdated numbers

- Providing incorrect information

How to Avoid These Mistakes

To prevent errors, always double-check the ABA Number before initiating a transaction. Keep your information up-to-date and verify the number with your bank if you're unsure.

Recent Updates and Changes in ABA Numbers

The ABA Number system continues to evolve to meet the demands of modern banking. Recent updates include enhanced security measures and improved compatibility with digital platforms.

Future Developments

As technology advances, the ABA Number system may incorporate new features to enhance security and efficiency. Staying informed about these changes will help you make the most of your banking experience.

Frequently Asked Questions about ABA Numbers

Q1: Can I use the same ABA Number for all my accounts?

In most cases, yes. However, some banks may assign different ABA Numbers for different types of accounts, such as checking and savings.

Q2: What happens if I enter the wrong ABA Number?

Entering the wrong ABA Number can result in failed transactions or funds being sent to the wrong account. Always verify the number before proceeding.

Q3: Are ABA Numbers used internationally?

No, ABA Numbers are specific to the United States. For international transactions, you may need to use a SWIFT code or IBAN.

Conclusion

Understanding the ABA Number is essential for anyone involved in banking transactions. From its historical significance to its modern applications, this unique identifier plays a critical role in ensuring the accuracy and security of financial operations.

We encourage you to share this article with others who may benefit from learning about ABA Numbers. For more insights into banking and finance, explore our other articles on our website. If you have any questions or feedback, feel free to leave a comment below.

Data Sources: