Bank ABA numbers play a crucial role in the financial system, enabling seamless transactions between banks. Whether you're transferring funds, setting up direct deposits, or paying bills, understanding what an ABA number is and how it works is essential for managing your finances effectively. In this article, we will explore everything you need to know about ABA numbers, including their purpose, structure, and usage.

Many people encounter ABA numbers when dealing with banking transactions but are unsure of their significance. These numbers are not just random digits; they serve as a unique identifier for banks in the United States, ensuring that money moves accurately and securely. As we delve deeper into this topic, you'll gain a comprehensive understanding of how ABA numbers function in the modern banking landscape.

This guide is designed to provide valuable insights into the importance of ABA numbers, their role in financial transactions, and how to locate them on your checks or bank statements. Whether you're a business owner or an individual managing personal finances, having a clear grasp of ABA numbers can help you navigate the banking system with confidence.

What is an ABA Number?

An ABA number, also known as a routing transit number (RTN), is a nine-digit code assigned to financial institutions in the United States. It serves as a unique identifier that helps banks and credit unions process transactions efficiently. The American Bankers Association (ABA) introduced this numbering system in 1910 to streamline the check-clearing process.

Key Features of ABA Numbers

ABA numbers are essential for various financial operations, including:

- Transferring funds between banks

- Setting up direct deposits for salaries or government benefits

- Paying bills through automatic payment systems

- Facilitating wire transfers

Each bank or credit union has its own ABA number, ensuring that transactions are routed to the correct institution. This numbering system has evolved over the years to accommodate the growing complexity of the financial industry.

History and Origin of ABA Numbers

The concept of ABA numbers dates back to the early 20th century when the American Bankers Association sought to standardize the banking system. Before the introduction of ABA numbers, processing checks was a cumbersome and error-prone process. The ABA worked with the Federal Reserve to develop a numbering system that would improve efficiency and accuracy.

Evolution of the System

Over the decades, the ABA numbering system has undergone several changes to meet the demands of modern banking:

- Expansion to include credit unions and non-bank financial institutions

- Adaptation to electronic payment systems

- Incorporation of security measures to prevent fraud

Today, ABA numbers remain a cornerstone of the U.S. banking infrastructure, facilitating millions of transactions every day.

Structure of an ABA Number

An ABA number consists of nine digits, each with a specific purpose. Understanding the structure of an ABA number can help you verify its authenticity and ensure accurate transactions.

Breaking Down the Nine Digits

- First four digits: Represent the Federal Reserve Routing Symbol

- Fifth and sixth digits: Identify the bank's geographic location

- Seventh digit: Indicates the Federal Reserve district where the bank is located

- Eighth and ninth digits: Act as a checksum to validate the number

This systematic arrangement ensures that ABA numbers are unique and error-free. Banks use sophisticated algorithms to generate and verify these numbers, minimizing the risk of mistakes during transactions.

How Are ABA Numbers Used?

ABA numbers are integral to various financial activities. Whether you're transferring money domestically or setting up recurring payments, these numbers ensure that funds reach the intended destination without delays or errors.

Common Uses of ABA Numbers

- Domestic Wire Transfers: Facilitate secure and swift transfers between U.S. banks

- Direct Deposits: Enable employers and government agencies to deposit funds directly into your account

- Bill Payments: Allow you to automate payments for utilities, loans, and other recurring expenses

By providing the correct ABA number, you can avoid common issues such as delayed transactions or misdirected funds. It's essential to double-check the number before initiating any financial operation.

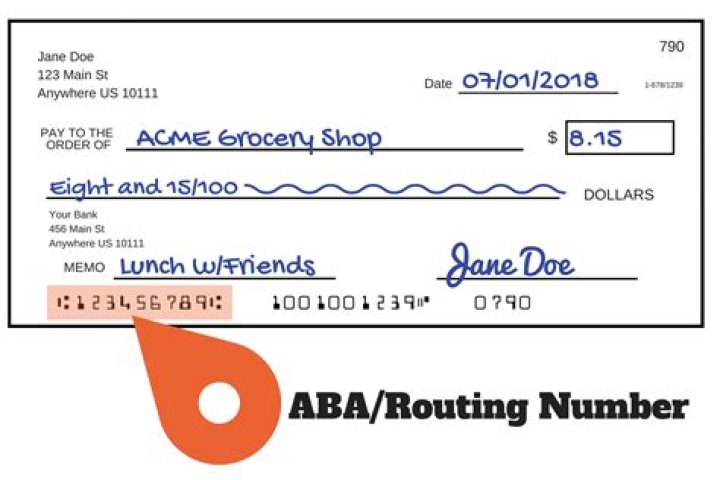

Where to Find Your ABA Number

Locating your ABA number is straightforward. Banks typically display this information on your checks, bank statements, and online banking portals. Knowing where to find your ABA number can save you time and prevent unnecessary complications.

Methods to Locate Your ABA Number

- On Your Checks: The ABA number is usually the first set of numbers at the bottom-left corner

- Bank Statements: Look for the routing number section in your monthly statement

- Online Banking: Access your account details through your bank's website or mobile app

If you're unsure about your ABA number, contact your bank's customer service for clarification. They can provide you with the correct number and guide you through any related processes.

ABA Number vs Routing Number

Many people use the terms "ABA number" and "routing number" interchangeably, but there are subtle differences between the two. While both serve similar purposes, their usage can vary depending on the context.

Key Differences

ABA numbers are primarily used for domestic transactions within the United States, whereas routing numbers can also be employed for international transfers. Additionally, some banks may have separate ABA numbers for wire transfers and direct deposits, so it's important to confirm which number to use for each transaction.

For clarity, always verify the specific requirements of the transaction you're conducting. Your bank can provide guidance on which number to use based on the nature of the transfer.

Security Features of ABA Numbers

Security is a top priority in the banking industry, and ABA numbers are no exception. Banks employ various measures to protect these numbers from fraud and unauthorized use.

How Banks Ensure ABA Number Security

- Checksum Validation: A mathematical formula verifies the authenticity of the number

- Encryption: Transactions involving ABA numbers are encrypted to prevent interception

- Authentication Protocols: Banks use multi-factor authentication to safeguard sensitive information

By implementing these security features, banks ensure that ABA numbers remain a reliable tool for conducting financial transactions.

Benefits of Using ABA Numbers

The use of ABA numbers offers numerous advantages for both individuals and businesses. These numbers streamline the banking process, reduce errors, and enhance the overall efficiency of financial operations.

Advantages of ABA Numbers

- Accuracy: Ensures funds are routed to the correct bank account

- Speed: Facilitates faster transactions compared to manual processing

- Convenience: Enables automated payments and direct deposits

These benefits make ABA numbers an indispensable tool in the modern banking system, empowering users to manage their finances with ease and confidence.

Common Challenges with ABA Numbers

While ABA numbers are generally reliable, users may encounter challenges when using them. Understanding these issues can help you address them proactively and avoid potential complications.

Potential Problems

- Incorrect Number Entry: Typing errors can lead to failed transactions

- Outdated Information: Banks may change their ABA numbers, requiring updates

- Fraudulent Use: Scammers may attempt to misuse ABA numbers for illegal activities

To mitigate these risks, always double-check the ABA number before initiating a transaction and stay vigilant against phishing attempts or suspicious requests.

Frequently Asked Questions About ABA Numbers

Here are some common questions people have about ABA numbers, along with their answers:

Q: Can I use my ABA number for international transactions?

A: ABA numbers are primarily used for domestic transactions within the United States. For international transfers, you may need a SWIFT code or IBAN.

Q: How do I know if my ABA number is correct?

A: Verify the number by checking your checks, bank statements, or online banking portal. You can also contact your bank for confirmation.

Q: What happens if I enter the wrong ABA number?

A: Incorrect ABA numbers can result in failed transactions or funds being sent to the wrong account. Always double-check the number before proceeding.

Conclusion

In conclusion, ABA numbers are a vital component of the U.S. banking system, enabling secure and efficient financial transactions. By understanding their purpose, structure, and usage, you can navigate the banking landscape with greater confidence and precision. Whether you're transferring funds, setting up direct deposits, or paying bills, ABA numbers ensure that your transactions are handled accurately and promptly.

We encourage you to share this article with others who may benefit from learning about ABA numbers. If you have any questions or feedback, please leave a comment below. Additionally, explore our other articles for more insights into personal finance and banking solutions.