In today's digital age, the ABA bank code plays a crucial role in facilitating seamless financial transactions. Whether you're transferring money domestically or internationally, understanding the ABA routing number is essential. This unique nine-digit code ensures that your funds reach the intended recipient without any errors.

The ABA bank code, also known as the routing transit number (RTN), serves as a digital address for banks and financial institutions. It helps identify the specific bank branch involved in the transaction, ensuring accuracy and efficiency. As we delve deeper into this topic, you'll discover how ABA codes work, their importance, and how to locate them effortlessly.

For individuals and businesses alike, having a clear understanding of ABA bank codes can streamline financial operations. From payroll processing to direct deposits, the ABA code plays a vital role in ensuring timely and secure transactions. Let's explore this topic further and uncover everything you need to know about ABA bank codes.

What is an ABA Bank Code?

The ABA bank code, officially known as the American Bankers Association routing transit number (ABA RTN), is a nine-digit numerical code assigned to financial institutions in the United States. It serves as a unique identifier for banks and credit unions, ensuring that funds are routed to the correct institution during transactions. This code was first introduced in 1910 by the American Bankers Association to standardize banking operations.

Primary Functions of ABA Codes

ABA codes perform several critical functions in the financial ecosystem:

- Facilitating electronic funds transfers (EFTs).

- Enabling direct deposits for payroll and government benefits.

- Supporting check processing and clearing.

- Providing a secure and reliable system for interbank communications.

History of ABA Code

The history of the ABA bank code dates back to the early 20th century when the American Bankers Association sought to create a standardized system for banking transactions. Initially, the code was used primarily for check processing. Over the years, its scope expanded to include electronic transactions, making it an indispensable part of modern banking.

Key Milestones in ABA Code Development

- 1910: Introduction of the ABA routing transit number.

- 1950s: Adoption of magnetic ink character recognition (MICR) for automated check processing.

- 1970s: Expansion to support electronic funds transfers (EFTs).

- 2000s: Integration with digital banking systems for enhanced security and efficiency.

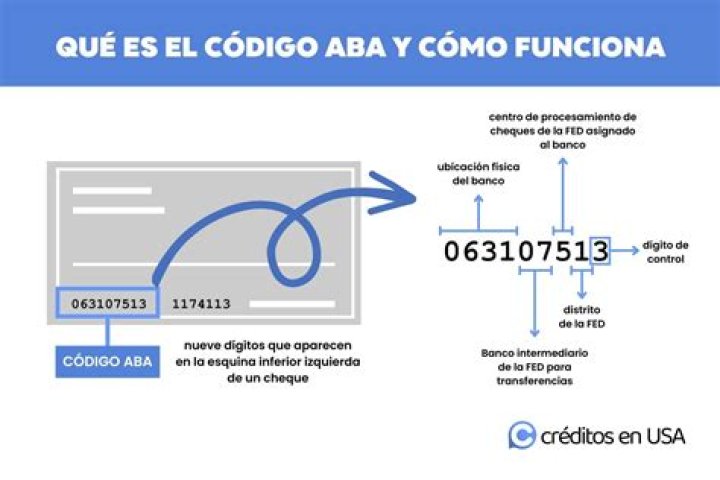

Structure of ABA Code

An ABA code consists of nine digits, each with a specific purpose:

- First four digits: Represent the Federal Reserve routing symbol.

- Fifth and sixth digits: Identify the American Bankers Association institution identifier.

- Seventh digit: Indicates the Federal Reserve check processing center assigned to the bank.

- Eighth digit: Denotes the state or region where the bank is located.

- Ninth digit: Acts as a check digit to verify the accuracy of the code.

How to Find Your ABA Bank Code

Locating your ABA bank code is a straightforward process. Here are the most common methods:

Methods to Find Your ABA Code

- Check your checks: The ABA code is printed at the bottom-left corner of your checks.

- Bank statement: Your monthly bank statement may include the ABA code.

- Online banking: Access your bank's website or mobile app to find the ABA code in your account settings.

- Bank website: Most banks provide ABA codes on their official websites.

Importance of ABA Bank Code

The ABA bank code is vital for ensuring the accuracy and security of financial transactions. Its primary importance lies in:

- Preventing errors in fund transfers.

- Enhancing the speed of electronic transactions.

- Providing a standardized system for interbank communication.

Impact on Business Transactions

For businesses, the ABA code is essential for payroll processing, vendor payments, and tax filings. It ensures that all financial transactions are executed smoothly and efficiently, reducing the risk of delays or errors.

Difference Between ABA and SWIFT Codes

While both ABA and SWIFT codes are used in banking, they serve different purposes:

Key Differences

- ABA Codes: Used primarily for domestic transactions within the United States.

- SWIFT Codes: Facilitate international wire transfers and are used globally.

Understanding the distinction between these codes is crucial for individuals and businesses engaging in cross-border transactions.

Common Uses of ABA Bank Codes

ABA bank codes are widely used in various financial activities, including:

Primary Applications

- Direct deposits for salaries and government benefits.

- Automated clearing house (ACH) transactions.

- Bill payments and recurring payments.

- Wire transfers within the United States.

Security Aspects of ABA Bank Codes

ABA bank codes are designed with security in mind. The inclusion of a check digit ensures the accuracy of the code, reducing the risk of errors. Additionally, financial institutions implement robust security measures to protect sensitive information associated with ABA codes.

Best Practices for Security

- Never share your ABA code with unauthorized individuals.

- Use secure platforms for transmitting ABA codes.

- Regularly monitor your bank accounts for unauthorized transactions.

Troubleshooting ABA Code Issues

If you encounter issues with your ABA bank code, here are some steps to resolve them:

- Verify the accuracy of the ABA code.

- Contact your bank's customer service for assistance.

- Check for updates or changes in your bank's ABA code.

The Future of ABA Bank Codes

As technology continues to evolve, the role of ABA bank codes may expand to accommodate new financial systems and platforms. The integration of blockchain and digital currencies could lead to innovations in how ABA codes are utilized. However, their fundamental purpose of ensuring secure and accurate transactions will remain unchanged.

Emerging Trends

- Increased adoption of digital payment systems.

- Enhanced security protocols for ABA codes.

- Integration with global financial networks.

Conclusion

In conclusion, the ABA bank code is a critical component of the modern financial system. Its role in facilitating accurate and secure transactions cannot be overstated. By understanding how ABA codes work and their various applications, individuals and businesses can optimize their financial operations.

We invite you to share your thoughts and experiences with ABA bank codes in the comments section below. Additionally, feel free to explore other informative articles on our website for more insights into the world of finance. Together, let's build a more informed and secure financial future!