Routing numbers and ABA numbers are terms often used interchangeably in banking, but do they mean the same thing? Understanding the distinction is crucial for anyone managing their finances, especially when it comes to transferring funds or setting up direct deposits. This article aims to demystify these terms and provide clarity on their usage.

In today's digital age, where banking transactions are increasingly done online, knowing the ins and outs of routing numbers can save you time and potential headaches. Whether you're setting up a direct deposit, paying bills online, or transferring money, understanding routing numbers is essential.

This guide will delve into the intricacies of routing numbers, their relationship with ABA numbers, and provide practical tips for using them effectively. By the end, you'll have a solid grasp of these financial tools and how they impact your banking activities.

What is a Routing Number?

A routing number, also known as a routing transit number (RTN), is a nine-digit code used in the United States to identify financial institutions during transactions. It plays a crucial role in ensuring that money moves efficiently between banks and credit unions. This number is essential for processes such as direct deposits, wire transfers, and check processing.

Routing numbers were first introduced in 1910 by the American Bankers Association (ABA) to streamline the growing volume of check transactions. Over the years, their usage has expanded to include electronic transactions, making them a cornerstone of modern banking infrastructure.

How Routing Numbers Work

Routing numbers function as a unique identifier for banks and financial institutions. They ensure that funds are directed to the correct institution during transactions. Each bank or credit union has its own routing number, which is specific to its geographical location and branch.

- First four digits: Represent the Federal Reserve Routing Symbol.

- Next four digits: Identify the bank or financial institution.

- Ninth digit: A check digit used for validation purposes.

Is a Routing Number the Same as an ABA Number?

The terms "routing number" and "ABA number" are often used synonymously because they refer to the same nine-digit code. The American Bankers Association (ABA) developed this numbering system, which is why the term "ABA number" is widely recognized. However, it's important to note that while they are the same, the context in which they are used may vary slightly.

Historical Context

The ABA introduced routing numbers in 1910 to standardize the processing of checks. Over time, the system evolved to accommodate electronic transactions, leading to the widespread use of routing numbers in digital banking. This historical connection is why both terms are still in use today.

Functions of a Routing Number

Routing numbers serve several critical functions in the banking system. They are essential for:

- Direct deposits: Ensuring payroll and other payments are sent to the correct account.

- Check processing: Facilitating the clearance of checks between banks.

- Wire transfers: Directing funds to the intended recipient's bank.

- Automated Clearing House (ACH) transactions: Handling recurring payments and transfers.

Each of these functions relies on the accuracy and integrity of routing numbers to ensure seamless financial operations.

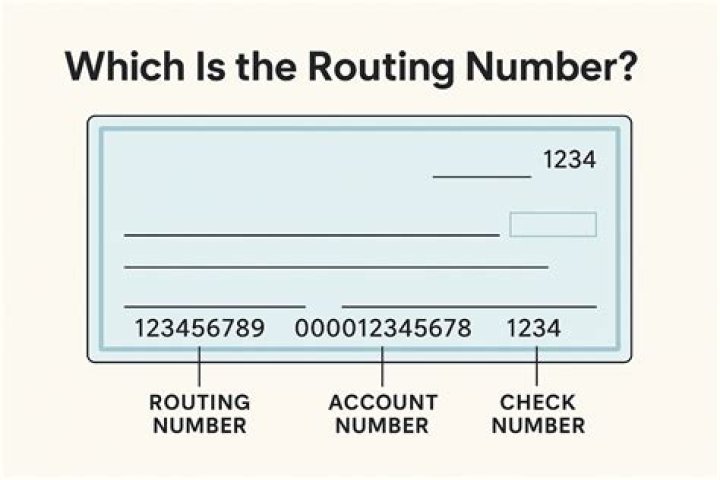

How to Find Your Routing Number

Finding your routing number is straightforward. Here are several methods you can use:

On Your Checks

The routing number is typically located at the bottom left corner of your checks. It is the first set of numbers in a series of three codes.

Online Banking

Most banks provide your routing number through their online banking portals. Simply log in to your account and navigate to the account information section.

Bank's Website

Many banks list their routing numbers on their official websites. A quick search on the bank's site should yield the necessary information.

Key Differences Between Routing and ABA Numbers

While routing numbers and ABA numbers are essentially the same, there are subtle differences in their usage:

- Context: "ABA number" is often used in formal or historical contexts, while "routing number" is more commonly used in everyday banking.

- Purpose: ABA numbers were originally designed for check processing, whereas routing numbers now encompass a broader range of transactions.

Understanding these nuances can help you communicate more effectively with your bank or financial institution.

Common Uses of Routing Numbers

Routing numbers are integral to various banking activities. Here are some of the most common uses:

Direct Deposits

Setting up direct deposits for payroll, Social Security benefits, or other recurring payments requires your routing number. This ensures that funds are deposited into the correct account.

Wire Transfers

When initiating a wire transfer, you'll need to provide your bank's routing number to ensure the funds reach the intended recipient.

ACH Transactions

Automated Clearing House (ACH) transactions, such as bill payments and recurring transfers, also rely on routing numbers to function smoothly.

Security Considerations for Routing Numbers

While routing numbers are not as sensitive as account numbers, they should still be protected to prevent unauthorized access. Here are some security tips:

- Keep your checks in a secure location.

- Do not share your routing number unless it is necessary for a legitimate transaction.

- Monitor your bank statements regularly for any suspicious activity.

By following these precautions, you can safeguard your financial information and reduce the risk of fraud.

The History of Routing Numbers

The history of routing numbers dates back to 1910 when the American Bankers Association introduced them to standardize check processing. Initially, they were used exclusively for check clearance, but their utility expanded with the advent of electronic banking. Today, routing numbers are a vital component of the U.S. banking system, facilitating millions of transactions daily.

Routing vs. SWIFT vs. IBAN

While routing numbers are specific to the U.S., other countries use different systems for international transactions. Here's a comparison:

SWIFT Codes

SWIFT codes, or Bank Identifier Codes (BIC), are used for international wire transfers. They consist of 8-11 characters and identify banks globally.

IBAN Numbers

International Bank Account Numbers (IBAN) are used in conjunction with SWIFT codes for international transactions. They provide a standardized way of identifying bank accounts across borders.

Understanding these differences is crucial for anyone engaging in global banking activities.

Tips for Managing Your Routing Number

Managing your routing number effectively can enhance your banking experience. Here are some practical tips:

- Keep a record of your routing number in a secure location.

- Double-check the routing number before initiating any transaction to avoid errors.

- Stay informed about any changes to your bank's routing number, as mergers or acquisitions may affect it.

By following these tips, you can ensure smooth and secure transactions.

Conclusion

In summary, routing numbers and ABA numbers are essentially the same, serving as a crucial component of the U.S. banking system. They facilitate a wide range of transactions, from direct deposits to wire transfers, ensuring that funds are directed to the correct accounts. Understanding their functions and usage can greatly enhance your banking experience.

We encourage you to share this article with others who may benefit from this information. If you have any questions or comments, feel free to leave them below. Additionally, explore our other articles for more insights into personal finance and banking.