Buying a home is one of the most significant financial decisions you will ever make, and understanding Chase home loan requirements is crucial for success. Whether you're a first-time homebuyer or a seasoned property owner, navigating the mortgage process can be overwhelming. This article will walk you through everything you need to know about Chase home loan requirements, ensuring you are well-prepared to secure the best mortgage for your needs.

Chase Bank, one of the largest financial institutions in the United States, offers a variety of home loan options tailored to meet different financial goals. However, meeting their specific requirements is essential to qualify for these loans. From credit scores to income verification, this guide will break down each requirement in detail.

By the end of this article, you'll have a clear understanding of what Chase expects from borrowers, how to improve your chances of approval, and the steps you need to take to secure your dream home. Let’s dive in!

Biography of Chase Bank

Chase Bank, a division of JPMorgan Chase & Co., is one of the largest banks in the United States. It has been serving customers for over 200 years, providing a wide range of financial services, including home loans. Below is a brief overview of the bank's history and its significance in the mortgage industry.

| Founder | Alexander Hamilton |

|---|---|

| Year Established | 1799 |

| Headquarters | New York City, NY |

| CEO | Jamie Dimon |

| Assets | Over $4 trillion |

Why Choose Chase for Your Home Loan?

Chase Bank offers competitive interest rates, flexible loan options, and a user-friendly application process. With a strong reputation for customer service, Chase is an excellent choice for those seeking a reliable mortgage lender.

Types of Chase Home Loans

Chase provides several types of home loans to cater to various financial situations and needs. Understanding these options is the first step in determining which loan is right for you.

Conventional Loans

Conventional loans are not backed by government programs. Chase offers conventional fixed-rate and adjustable-rate mortgages, making them suitable for borrowers with strong credit histories.

FHA Loans

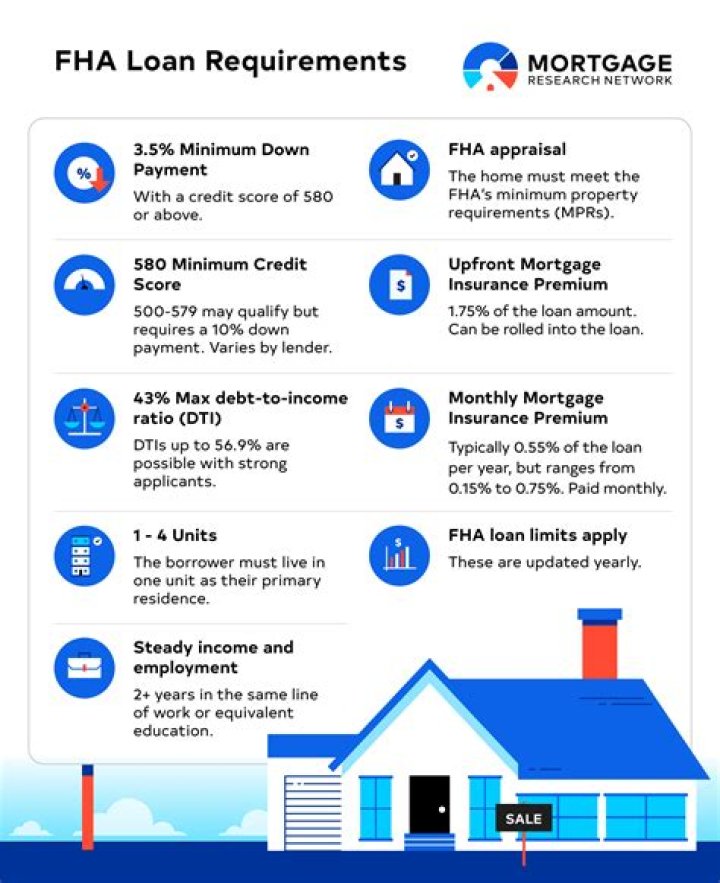

FHA loans are insured by the Federal Housing Administration and are ideal for first-time homebuyers or those with lower credit scores. Chase offers FHA loans with competitive terms.

VA Loans

VA loans are available to eligible veterans, active-duty service members, and surviving spouses. Chase provides VA loans with no down payment requirement.

USDA Loans

USDA loans are designed for rural property buyers and offer 100% financing. Chase participates in the USDA loan program, making it accessible to eligible borrowers.

Chase Home Loan Credit Score Requirements

Your credit score plays a critical role in determining your eligibility for a Chase home loan. Here’s what you need to know:

- Conventional loans typically require a credit score of at least 620.

- FHA loans may accept scores as low as 580, depending on the down payment.

- VA loans generally require a score of around 620, though this can vary.

- USDA loans usually require a minimum score of 640.

Improving your credit score can significantly increase your chances of approval and help you secure better interest rates.

Income Requirements for Chase Home Loans

Chase evaluates your income to ensure you can afford your mortgage payments. Here’s how they assess your income:

Documentation Needed

- Recent pay stubs (typically covering the last 30 days).

- W-2 forms for the past two years.

- Bank statements for the past two months.

Self-employed borrowers may need to provide additional documentation, such as tax returns and profit-and-loss statements.

Chase Home Loan Down Payment Requirements

The down payment is a significant factor in securing a home loan. Chase’s down payment requirements vary depending on the loan type:

- Conventional loans typically require a down payment of 3-20%.

- FHA loans allow down payments as low as 3.5%.

- VA loans may require no down payment.

- USDA loans offer 100% financing.

Keep in mind that larger down payments can reduce your monthly mortgage payments and decrease the total cost of the loan.

Debt-to-Income Ratio Requirements

Your debt-to-income (DTI) ratio is another critical factor in Chase’s underwriting process. Here’s how it works:

Chase generally requires a DTI ratio of 43% or lower. However, borrowers with strong credit scores and other compensating factors may qualify with a higher DTI ratio. To calculate your DTI ratio, divide your total monthly debt payments by your gross monthly income.

Employment History Requirements

Chase evaluates your employment history to assess your financial stability. Here’s what they look for:

- At least two years of consistent employment in the same field or industry.

- Documentation of your employment history, such as pay stubs and W-2 forms.

- For self-employed borrowers, a detailed business history and financial records.

A stable employment history can improve your chances of approval and help you secure better loan terms.

Property Eligibility Criteria

Chase has specific criteria for the properties it will finance. Here’s what you need to know:

- The property must be used as your primary residence.

- It must meet appraisal standards and pass an inspection.

- Chase does not finance properties with significant structural issues.

Consult with a Chase mortgage specialist to ensure your desired property meets all eligibility requirements.

Additional Documentation Needed

Chase may request additional documentation depending on your financial situation and loan type. Common documents include:

- Proof of homeowners insurance.

- Gift letters if receiving down payment assistance.

- Bankruptcy discharge papers if applicable.

Providing all required documentation promptly can expedite the loan approval process.

Chase Home Loan Application Process

Applying for a Chase home loan involves several steps. Here’s a breakdown of the process:

Step 1: Pre-Approval

Start by getting pre-approved for a mortgage. This involves submitting basic financial information and receiving a conditional loan approval.

Step 2: Property Selection

Once pre-approved, begin searching for your dream home. Work with a real estate agent to find a property that meets Chase’s eligibility criteria.

Step 3: Loan Processing

After selecting a property, Chase will begin processing your loan application. This includes verifying your income, credit score, and other financial details.

Step 4: Closing

The final step is closing on your loan. At this stage, you’ll sign all necessary documents and pay any closing costs. Congratulations, you’re now a homeowner!

Tips for Meeting Chase Home Loan Requirements

Here are some tips to help you meet Chase home loan requirements:

- Improve your credit score by paying bills on time and reducing debt.

- Save for a larger down payment to reduce your loan amount and monthly payments.

- Maintain a stable employment history and avoid changing jobs during the application process.

- Gather all required documentation in advance to streamline the application process.

Conclusion

Understanding Chase home loan requirements is essential for securing the best mortgage for your needs. From credit scores to income verification, each requirement plays a crucial role in the approval process. By following the tips outlined in this guide, you can increase your chances of approval and secure a favorable loan.

We encourage you to take action by applying for pre-approval or consulting with a Chase mortgage specialist. Don’t forget to share this article with others who may find it helpful and explore more resources on our website. Happy homebuying!